For this issue of Manager of the Month we explore the newer middle market firm, Avesi Partners

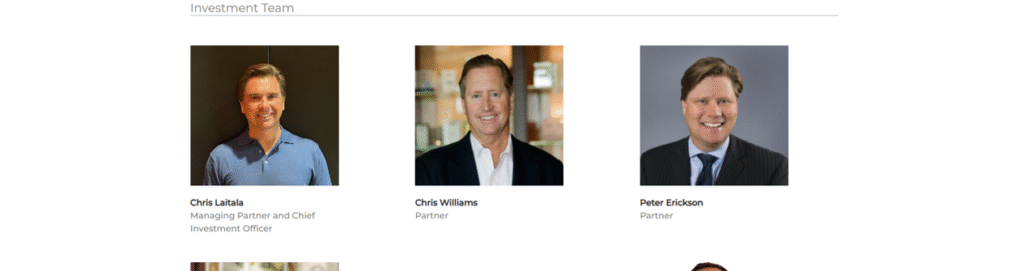

Avesi Partners (“Avesi”) is a relatively new North American private equity firm, founded in 2021 by Chris Laitala, formerly a partner at Lindsey Goldberg and prior to this H.I.G, where he built very compelling track records. Chris Laitala was joined by Chris Williams, co-founder of Harris Williams, a prominent M&A advisory firm, and Peter Erickson, who spent over 20 years at TripleTree, a leading healthcare investment bank. This senior team was joined more recently in 2023, by partner and COO John Aiello, who had also served as a partner at Lindsay Goldberg and previously as a managing director at Goldman Sachs.

The firm has made a running start, despite its emerging nature, having raised two oversubscribed funds to date. The most recent being a $1.35 billion Fund II, raised in 2024, with strong backing from existing and new LPs, including family offices, funds of funds and PE consultants. The name “Avesi” itself, is derived from the Finnish word for “water,” symbolizing a journey of growth and the firm’s mission to provide an essential source of expansion to its partners and portfolio companies.

Beneath the four partners sits a well-resourced and growing team, based primarily in Stamford, CT, but also Richmond, VA. The firm boasts a solid junior base of associates and vice presidents, but has recently concentrated on growing the more senior, ‘second layer’, hiring managing director Seth Person (formerly of York Private Equity) to sit alongside existing MD, Pete Tedesco.

Strategy

Avesi focuses on control buyouts in the North American lower middle market (“LMM”), though aiming for meaningful management/founder ownership alongside. The firm focuses exclusively on healthcare and business services companies with $5-30 million of EBITDA. Select investments include:

- Danforth Advisors (Fund I) a provider of financial and operational support to life science companies. It spans wide-ranging needs, whether short or long term, including accounting and operational finance support, capital raising, financial planning and analysis, IPO preparation, post-public SEC compliance, clinical business operations management and strategic and operational human resources.

- Memory Blue (Fund I) a provider of outsourced B2B sales development services to technology companies in US, EMEA and APAC. In addition to providing outsourced sales development, MemoryBlue provides clients with a direct hire offering, focused on placing candidates directly into technology sales roles and a sales training service known as “Academy”.

- PointQuest (Fund I) a provider of adolescent behavioural health and special education services in California, primarily serving K-12 school districts. The company offers a full continuum of special education services by providing speech language pathologists, occupational therapists, mental health therapists, paraprofessionals. and other specialists.

Avesi’s strategy operates around its “Buy Well, Build Well, Sell Well” mantra. At the onset, the firm focuses on relative valuation, aiming to acquire companies at attractive multiples relative to comparable transactions (often around a 25% discount). Avesi aims to be a first or early mover in a sub-sector, primarily by developing market themes before initiating targeted searches for businesses in a researched sub-vertical, both through investment professionals and the dedicated business development function. Ideally, deals are proprietary, but where the team does participate in competitive transactions, it aims to pre-empt the process and must see evidence of multiple arbitrage at exit in either that space, or analogous spaces.

Target portfolio companies typically exhibit strong organic growth, shown consistently over at least the last three years, and must offer further avenues of organic growth over the lifetime of Avesi’s hold. Founder or management rollover is key, with alignment of interests being a core pillar of value creation. Avesi primarily aims to scale the organic element of the business, though does opportunistically utilise M&A to achieve strategic objectives. The end result being a professionalised, organically grown company, typically exhibiting around $50 million in EBITDA, which is attractively positioned and more strategically important to own for either larger private equity firms or strategics.

Performance

Avesi has made a very strong start in its Fund I (2021), with eight investments under its belt and compelling performance. That said, while the foundations in team and strategy are there, the funds remain very young and have yet to truly prove themselves.

Fundraising

Avesi Partners raised Fund I in 2021 with $875 million of committed capital. The fund was oversubscribed and closed above its original target of $650 million, just several months after launching. The team then closed Fund II in 2024 at $1.35 billion, also significantly oversubscribed, hitting the hard cap just months after launch with strong backing from existing and new LPs. As a result, Avesi won’t be back to market in the near future, but is certainly one to watch for the limited partner looking to back strong emerging GPs.

If you have a manager you think should be featured for “Manager of the Month”, or you are a GP and would like to be featured, reach out to contact@lpgateway.com with your suggestion.